RIAA Conference

Australia 2026

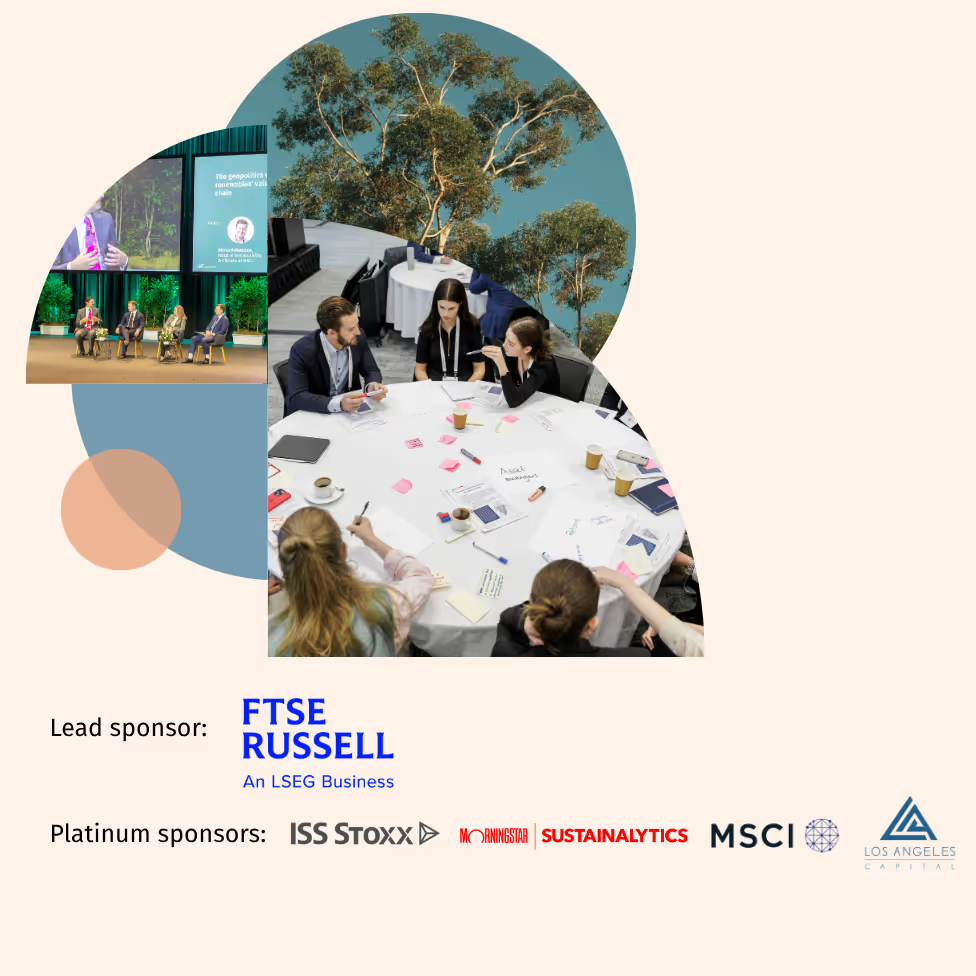

Join us on 27 & 28 May in Melbourne or online for the largest responsible investment gathering in the Southern Hemisphere. An immersive, hands-on program focused on the systems that underpin strong financial performance and how climate, nature, technology, governance and regulation intersect in practice.

The largest network of responsible and impact investors in AU & NZ

With 500+ members representing A$76 trillion / NZ$83 trillion in assets under management. RIAA is the largest and most active network of people and organisations engaged in responsible, ethical and impact investing across Australia and New Zealand.

Our membership includes super funds, KiwiSaver providers, fund managers, banks, consultants, researchers, brokers, impact investors, property managers, trusts, foundations, faith-based groups, financial advisers and individuals.

Our 500+ members include

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

.png)

About RIAA

The Responsible Investment Association Australasia (RIAA) is a not-for-profit organisation dedicated to ensuring capital is aligned with achieving a healthy society, environment and economy.

With 500+ members representing A$76 trillion / NZ$83 trillion in assets under management, RIAA is the largest and most active network of people and organisations engaged in responsible, ethical and impact investing across Australia and New Zealand.

Upcoming events straight to your inbox

Ngā Rauemi mō Te Ao Māori | Resources for Understanding the Māori World View

This collection of educational resources represents a comprehensive exploration of Te Ao Māori – the Māori world view - specifically developed to assist business, investment, and finance professionals in understanding and integrating Māori perspectives into their practice.